If you’re reading this and thinking, “didn’t we just do this?”—you’re not alone.

Last year, tariffs shook the first half of 2025 before markets found their footing and rallied to new highs. Now, just a few months into 2026, the playbook feels familiar. Escalating conflict with Iran has disrupted global energy markets, sent fertilizer and raw material costs climbing, and reintroduced financial market volatility. Different headlines, same volatility.

Here’s the good news: the US is energy independent, and we believe it should be well insulated from the supply chain shock we are seeing from the closure of the Strait of Hormuz. Emerging markets in Asia and Africa will most likely be the hardest hit economically – with European and developed markets in Asia not far behind. The US has been building capabilities to export natural gas. These projects are now coming online and, in our view, should help fill the void left by a lack of natural gas supply in the Middle East.

The diversified, goals-based portfolios we built aren’t designed to dodge every storm—they’re designed to weather them. Our positioning across alternatives, hedged equity, and fixed income is designed to help absorb the impact and keep your long-term plan on course.

The US economy surprised skeptics last year, powering through trade uncertainty to deliver strong corporate earnings and broadening market gains. We believe that same resilience is still at work beneath the surface, even as today’s headlines feel unsettling. There certainly will be bumps ahead, and we have adjusted portfolios accordingly.

Our team is actively monitoring the ripple effects of the Iran conflict, adjusting where it makes sense. If the second half of 2025 was any guide, patience and preparation historically rewarded those who stay the course.

Favorability Scale

The sliding scales below are meant to represent HFM’s current assessment of favorability of the market landscape in various investment areas as of the most recent quarter end. Our investment committee is looking to communicate to you a complicated thought process as simply as possible. The favorability scale considers the following factors: Current Yield, Growth, Value, and Market Conditions.

The information contained here should not be construed as a recommendation to purchase or sell any particular security or an assurance that any particular security held in a portfolio will remain in the portfolio or that a previously held security will not be repurchased. Securities discussed may not represent a portfolio’s specific or entire holdings. It should not be assumed that any security transactions or holdings discussed have been or will prove to be profitable or that future investment decisions will be profitable or will equal or exceed the investment performance of the securities or portfolios discussed.

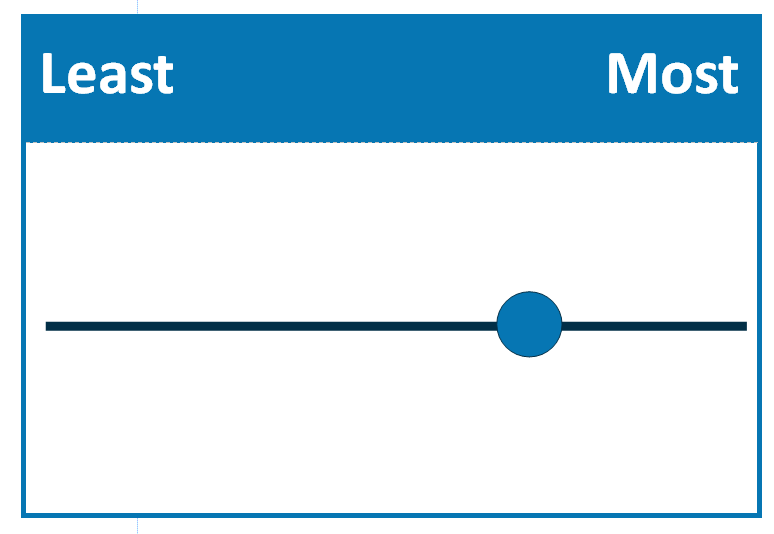

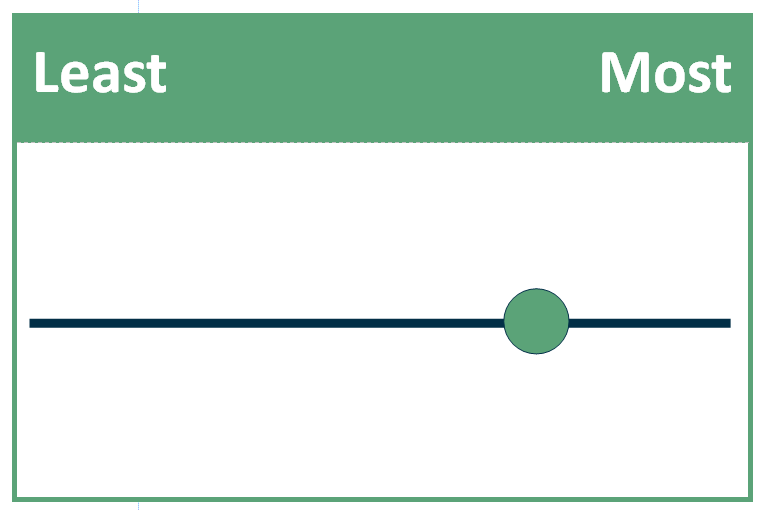

Equity Favorability

HFM Strategic Equity Positioning (Long Term)

Global equities have declined since the start of the conflict with Iran. The closing of the Strait of Hormuz, responsible for 20% of the world’s oil supply by the Iranian Republican Guard, has increased the cost of energy worldwide. The hardest hit regions are Asia, followed by Europe, and then North America. One key aspect we have used to decide in which countries to invest is the cost of energy and energy security. The regions with higher energy costs and greater reliance on energy imports have been the hardest hit economically. We remain MORE favorable on equities as they adapt to a challenging energy environment.

HFM Tactical Equity Positioning (Short Term)

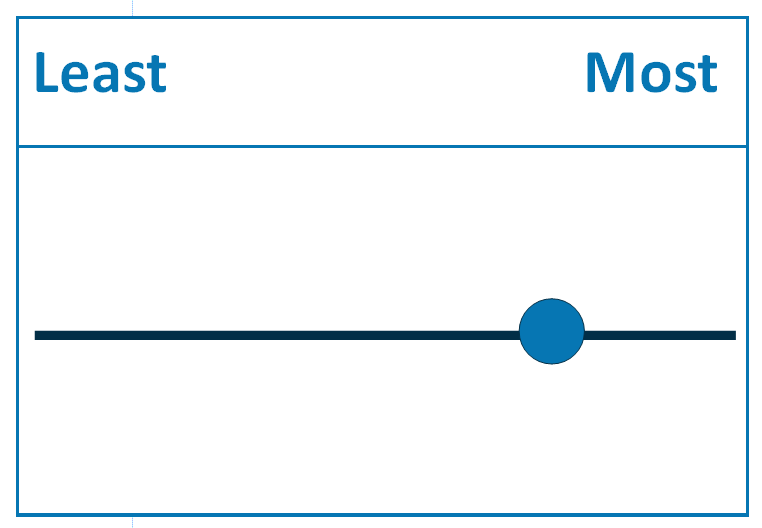

Large Cap

Large Caps remain attractively positioned; earnings growth is still expected to be double digits in 2026, and once the Iran conflict has been resolved the price of energy should settle back down to prewar levels. Consumer spending probably will be less robust given the higher cost of gasoline, trucking, and airline transportation. Offsetting this we hope will be the effects of the higher tax refunds. We remain MORE favorable in this segment.

Small Cap

Small Cap stocks have been more insulated from the energy shocks from Iran thus far. Expectations for Fed rate cuts have driven their performance. With the increase in energy prices, fewer cuts or none at all may be in the cards which would be negative for this asset class. We remain Neutral.

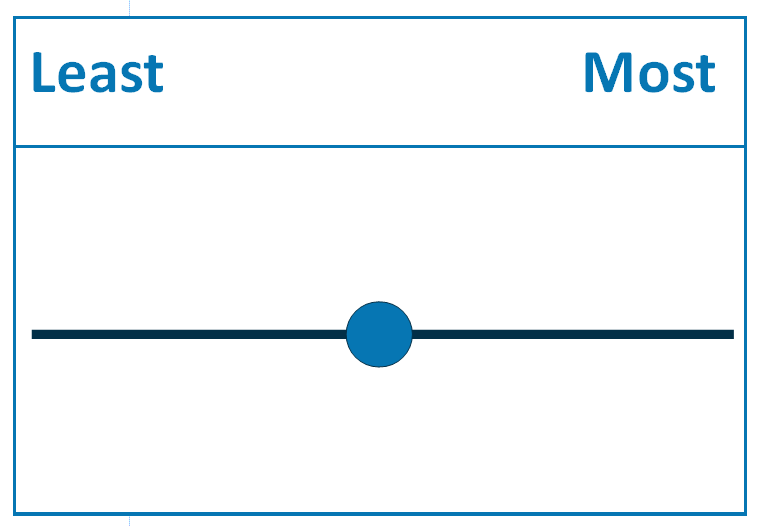

Cutting Edge

Enthusiasm around AI and innovation continues to normalize following strong gains in prior years. Markets have become increasingly selective, favoring companies with proven revenue growth while pulling back from more speculative names. We remain MORE favorable on this segment.

International

International had a strong start to the year, outperforming US stocks until the Iran conflict. Since the conflict they have suffered larger drawdowns vs their US brethren. Valuations remain more attractive, but paired with concern over energy costs and a stronger dollar, we remain NEUTRAL on this segment.

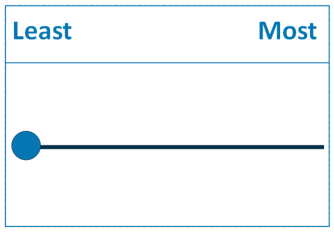

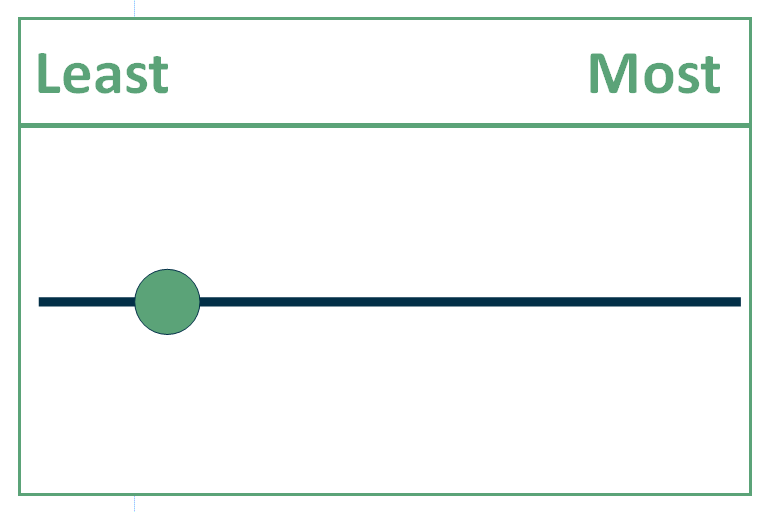

Hedged Equity

This segment has had a reduced exposure over the last few quarters. For now, we remain underexposed but we may reallocate the tactical strategy if weakness persists. We maintain our LEAST favorable outlook on this segment.

Fixed Income/Bonds Favorability

HFM Strategic Fixed Income Positioning (Long Term)

Overall, bond yields continued to grind lower during part of 1Q 2026 before reversing course and rising due to concerns about private credit, persistent inflation, and the potential for the Iran war to further increase inflation, along with renewed fiscal and economic policy uncertainty. An index proxy for US Investment Grade sector yields has risen ~40 bps (basis points) since this year’s February low. Overall, fixed income price and yield performance YTD in 1Q 2026 has been slightly negative. Generally, yields remain attractive, near to above 25-year historical average levels offering solid income earning opportunity. We continue to maintain a MORE favorable outlook on Fixed Income.

HFM Tactical Fixed Income Positioning (Short Term)

Investment Grade Bonds

Investment Grade sector yields remain at attractive levels above their 10-year and 25-year historical average levels. The portion of yield compensating for default, downgrade, and other risks remains below long-term average levels despite increasing since the start of the Iran war. Attractive starting all-in yield levels continue to offer favorable income generation and risk mitigation properties if e.g., the Iran conflict were to lead to stagflationary or recessionary economic outcomes. Attractive opportunities exist in the mortgage backed security, asset backed security, and select corporate bond areas. We maintain a MORE favorable outlook on Investment Grade bonds.

High Yield

High Yield sector yields are attractive near the 10-year and 25-year historical average levels, continuing to provide lower price sensitivity to rising rates/yields. However, the portion of yield compensating for default, downgrade, and other risks is below long term average levels despite increasing since the beginning of 1Q 2026. High Yield sector performance is sensitive to economic fundamentals and price movements are more closely aligned with equities. A prolonged conflict with Iran leading to deterioration of economic fundamentals or a recession raises downside performance risk for this sector. We maintain a bias for tactical allocations to higher quality, shorter maturity, favorably structured bonds and a LESS favorable outlook on the High Yield sector.

Alternatives Favorability

HFM Strategic Alternatives Positioning (Long Term)

The alternatives we use continue to perform well in periods of volatility. These funds continue to provide a positive return regardless of how equity and fixed income markets perform. We continue to see this area as MOST FAVORABLE and is a key tool to controlling volatility and solidifying financial plans.