Remember that feeling when you’re approaching the top of a rollercoaster, knowing the drop is coming but not quite sure when? That was Q2 2025 in a nutshell. And while the ride was wild, we strived to keep everyone securely fastened in their seats. The market started the year like a marathon runner saving energy for the final sprint – the S&P 500 quietly reached new heights on February 19th at 6,137. Then in April came “Liberation Day.” When the new tariff plans were announced, markets reacted violently – dropping 12% in a few short days, bottoming down 20% from their all-time highs. Amid this market chaos, various hedge funds which serve as a vital link between various financial markets were rumored to be failing. Their failure would certainly bring greater market turmoil across multiple financial markets. To date, it has remained just a rumor.

Focus on prudent risk management

Amidst this uncertain backdrop, our team decided the most prudent course of action was to control risk by doubling down on our hedged equity sleeve. These hedges were selected to protect your wealth if things got worse, while still letting you participate if markets recovered through the 90-day trade negotiation window announced by the Trump administration.

This market volatility was a stress test for our alternatives portfolio. These investments are designed to provide a consistent return regardless of market environment and we tweaked them upon the election of President Trump, a strategy to outperform other asset categories in a volatile environment.

To our surprise markets have recovered faster than expected. As we write this, markets have climbed back near their peaks – almost at the upper limit of what our hedging strategy allows. It’s like we put a safety net under a tightrope walker who ended up not needing it. We believe it was best to go with “better safe than sorry.”

Looking ahead

The coast isn’t clear yet. Trade negotiations are ongoing, and geopolitical risks have elevated further with the recent US bombing of Iranian nuclear facilities. The US economy remains on solid footing with labor markets still tight, and corporate profits looking solid.

Favorability Scale

The sliding scales below are meant to represent HFM’s current assessment of favorability of the market landscape in various investment areas as of the most recent quarter end. Our investment committee is looking to communicate to you a complicated thought process as simply as possible. The favorability scale considers the following factors: Current Yield, Growth, Value, and Market Conditions.

The information contained here should not be construed as a recommendation to purchase or sell any particular security or an assurance that any particular security held in a portfolio will remain in the portfolio or that a previously held security will not be repurchased. Securities discussed may not represent a portfolio’s specific or entire holdings. It should not be assumed that any security transactions or holdings discussed have been or will prove to be profitable or that future investment decisions will be profitable or will equal or exceed the investment performance of the securities or portfolios discussed.

Equity Favorability

HFM Strategic Equity Positioning (Long Term)

Markets have rebounded from earlier sell-offs. The economy remains resilient despite geopolitical tensions and trade war uncertainties. Strong earnings are supporting investor confidence. We remain MORE favorable in Q2.

HFM Tactical Equity Positioning (Short Term)

Large Cap

Large-cap stocks are benefiting from strong earnings and AI-driven optimism. Valuations are high, but performance justifies them so far, especially among mega-cap names. We remain MORE favorable on this segment.

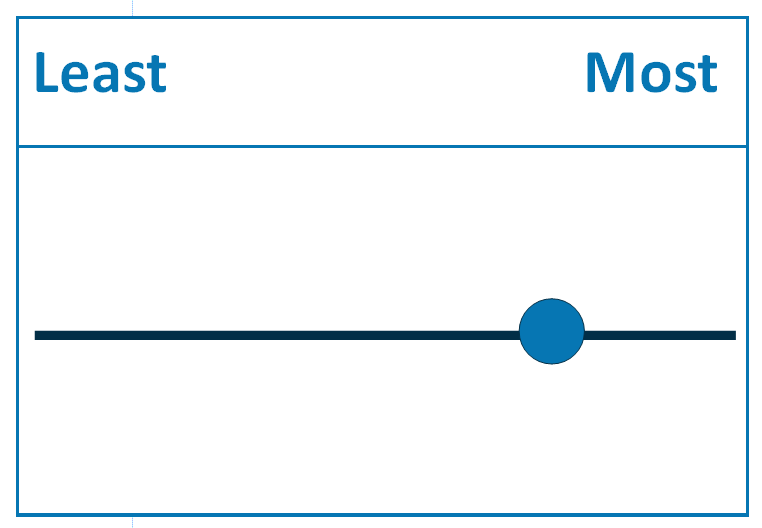

Small Cap

Small caps are underperforming in a high-interest rate environment. Valuations are cheaper than Large-cap stocks, but improvement likely depends on future Fed rate cuts. We remain LESS FAVORABLE on this segment.

Cutting Edge

AI-related investments are booming, with record capital spending. Nvidia’s strong earnings highlight sector strength. Valuations remain high. We remain NEUTRAL on this segment.

International

Tariff uncertainty and global tensions are concerns. A weaker dollar has helped international stocks outperform US stocks this year. We remain LESS favorable on this segment.

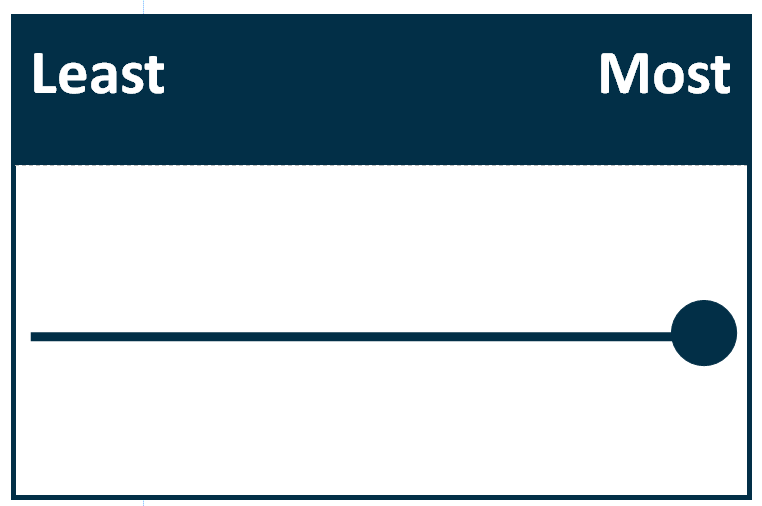

Hedged Equity

With increased market volatility, increased geopolitical risks, and continuous administration policy changes, the hedged equity strategy helps to reduce the downside market risks. We move to MOST favorable on the Hedged Equity segment in Q2.

Fixed Income/Bonds Favorability

HFM Strategic Fixed Income Positioning (Long Term)

Overall fixed income yields remain attractive at levels last experienced pre-Great Financial Crisis. Current yield levels reflect monetary, trade, and fiscal policy uncertainty and offer improved protection against the risk of rising yields resulting in price declines. We remain MORE favorable on Fixed Income.

HFM Tactical Fixed Income Positioning (Short Term)

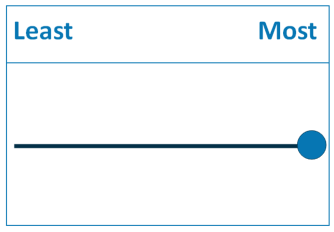

Investment Grade Bonds

Overall Investment Grade Fixed Income sector yield levels remain attractive in historical context above long-term historical average. However, the compensation for taking risk remains below the long-term historical average. We increase our outlook to MORE favorable on Investment Grade bonds.

High Yield

The High Yield sector continues to offer attractive yields, but investors are not duly compensated for potential downside risks if the economy slows down. We remain LESS favorable on High Yield bonds.

Alternatives Favorability

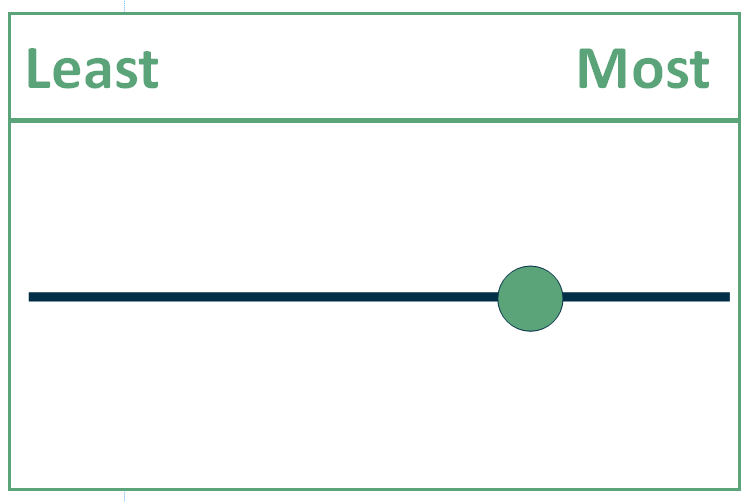

HFM Strategic Alternatives Positioning (Long Term)

The goal of our alternatives portfolio is to provide a positive return regardless of market environments. This quarter was a massive test of the strategy, and we are pleased with its excellent performance considering extremely volatile markets. We move to MOST favorable on this segment.