If last quarter felt like a rollercoaster ride, this quarter was the moment we caught our breath and found our footing again. After the dramatic “Liberation Day” sell-off in April that saw markets plunge 20% from their peaks, the third quarter delivered something we hadn’t seen in months: stability with a side of optimism.

The S&P 500’s recovery from its April lows has been nothing short of remarkable – climbing back to all-time highs by quarter end. What’s driving this renewed confidence? A combination of better-than-feared tariff outcomes, aggressive earnings revision cuts that set a low bar for companies to beat, and the Federal Reserve’s pivot toward more accommodative policy. Markets now expect the Fed to cut rates to around 3% by the end of 2026, a dramatic shift from barely pricing in any cuts just months ago.

Looking ahead

Labor markets look weaker in recent months, but the economy is chugging along fueled by the AI boom with its massive investments in data centers. Lower rates from the Federal Reserve have the potential to propel equities higher due to lower borrowing costs. Uncertainty around trade tensions remain and the complete costs of tariffs may have yet to hit the economy.

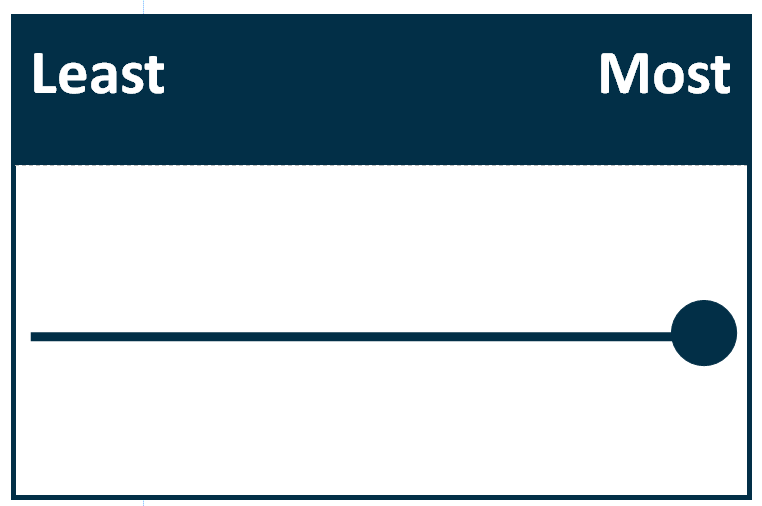

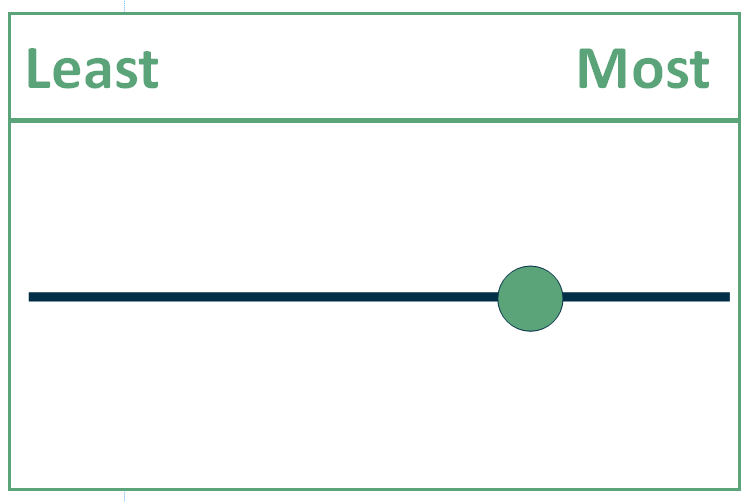

Favorability Scale

The sliding scales below are meant to represent HFM’s current assessment of favorability of the market landscape in various investment areas as of the most recent quarter end. Our investment committee is looking to communicate to you a complicated thought process as simply as possible. The favorability scale considers the following factors: Current Yield, Growth, Value, and Market Conditions.

The information contained here should not be construed as a recommendation to purchase or sell any particular security or an assurance that any particular security held in a portfolio will remain in the portfolio or that a previously held security will not be repurchased. Securities discussed may not represent a portfolio’s specific or entire holdings. It should not be assumed that any security transactions or holdings discussed have been or will prove to be profitable or that future investment decisions will be profitable or will equal or exceed the investment performance of the securities or portfolios discussed.

Equity Favorability

HFM Strategic Equity Positioning (Long Term)

While the pace of economic activity has cooled somewhat from earlier in the year, consumer spending has remained strong and the outlook for the economy in 2026 continues to look constructive given the large fiscal and tax bill that was passed by Congress in June. We remain MORE favorable in this segment.

HFM Tactical Equity Positioning (Short Term)

Large Cap

The S&P 500 is up more than 30% from the April tariff news lows (12% YTD). October is historically prone to volatility, so we could see a pullback at any time but earnings growth for 2026 looks good and any sell off should be short lived.We remain MORE favorable on this segment.

Small Cap

With the Federal Reserve lowering rates for the first time since 12/2024, things are starting to favor small caps in a lower rate environment. Small cap performance has rebounded well in Q3. We are now NEUTRAL on this segment.

Cutting Edge

While still being expensive the cutting edge sector of the technology sector continues to offer the best outlook for above average growth fueled by massive investments in cloud and AI infrastructure. We remain NEUTRAL on this segment.

International

International stocks performed well in Q3. If the dollar continues to weaken, we will consider shifting more to international equities. We are now NEUTRAL on this segment.

Hedged Equity

While valuations are now high for much of the market, the risk return of hedged equity positions do not offer the risk reward requisite to add to any positions. We are now LESS favorable on this segment.

Fixed Income/Bonds Favorability

HFM Strategic Fixed Income Positioning (Long Term)

Overall yield levels have been trending lower this year due to a combination of recent and expected future monetary policy easing and reductions in fiscal, economic, and trade policy uncertainty. Despite this decline, yields are above their 20-year averages and continue to generate solid income which can offset price declines if yields increase. The Fed resuming rate cuts are a supportive factor for fixed income. We maintain MORE favorable on Fixed Income.

HFM Tactical Fixed Income Positioning (Short Term)

Investment Grade Bonds

Overall Investment Grade Fixed Income sector yield levels remain attractive in historical context above long-term historical average despite the continuing trend of declining yields. However, the portion of yield compensating for taking default, downgrade, and other risks continues to trend down and is below long-term historical average. Higher quality Investment Grade bonds continue to offer attractive starting yields and can offer risk mitigating properties in potential recessionary or stagflationary-light economic environments. Continuing to be biased toward sectors offering greater compensation for taking default, downgrade, and other risks. We maintain a MORE favorable outlook on Investment Grade bonds.

High Yield

The High Yield sector continues to offer attractive absolute yields and lower sensitivity to the risk of rising yields. However, yields have continued to trend down and stand below long-term historical average. Similarly, compensation for default, downgrade, and other risks remains below long-term average, i.e., past 20+ years. Attractive yields are offset by greater downside performance risk should economic fundamentals deteriorate, or a recession occur. Bias to tactical allocations to high quality, shorter maturity, favorably structured bonds. We maintain a LESS favorable outlook on High Yield bonds.

Alternatives Favorability

HFM Strategic Alternatives Positioning (Long Term)

With equity markets becoming more expensive over the quarter, we see this asset class growing in importance to navigating potential volatility on the horizon. We remain the MOST favorable on Alternatives.