The first half of 2025 reminded us why building a resilient, diversified portfolio matters. Escalating tariffs delivered a shock to the global economic order, rattling markets, and testing investor nerves. Our alternatives, hedged equity, and fixed income holdings helped buffer the sudden downturn—an example of how diversification builds resilience when you need it most.

The second half of the year highlighted just how resilient the U.S. economy can be. While spring brought genuine anxiety, as trade tensions dominated headlines, calm in the stock market returned by summer. Stocks steadily climbed back to new highs with technology and artificial intelligence (AI) companies leading the way. AI has been the dominant theme for the year, but we were encouraged to see gains spread more broadly—banks, industrials, healthcare, and other sectors all had their moments in the sun.

If 2025 taught us anything, it’s that markets can handle more turbulence than we often give them credit for, but a diversified portfolio remains essential for navigating uncertain times.

Looking ahead to 2026, our outlook remains optimistic for equities as AI matures and its benefits spread to industries beyond technology. We continue to watch the labor market closely as it has softened of late. Corporate earnings remain strong with continued investment in AI leading the economy higher. With the Federal Reserve continuing to lower interest rates, we are hopeful for continued economic growth and a buoyant stock market.

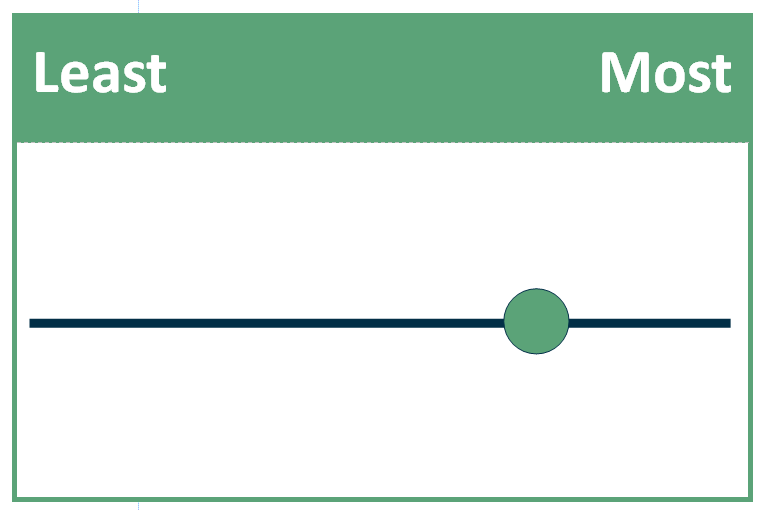

Favorability Scale

The sliding scales below are meant to represent HFM’s current assessment of favorability of the market landscape in various investment areas as of the most recent quarter end. Our investment committee is looking to communicate to you a complicated thought process as simply as possible. The favorability scale considers the following factors: Current Yield, Growth, Value, and Market Conditions.

The information contained here should not be construed as a recommendation to purchase or sell any particular security or an assurance that any particular security held in a portfolio will remain in the portfolio or that a previously held security will not be repurchased. Securities discussed may not represent a portfolio’s specific or entire holdings. It should not be assumed that any security transactions or holdings discussed have been or will prove to be profitable or that future investment decisions will be profitable or will equal or exceed the investment performance of the securities or portfolios discussed.

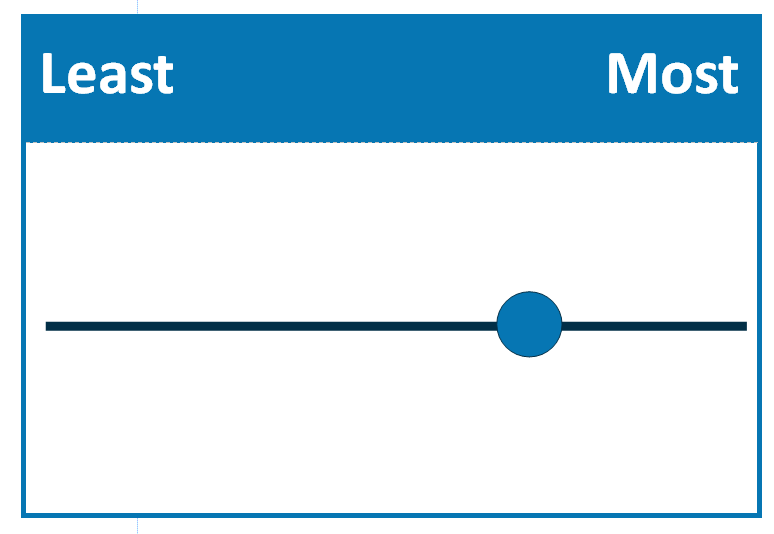

Equity Favorability

HFM Strategic Equity Positioning (Long Term)

U.S. stocks rose toward record highs in Q4 as investors priced in solid economic data and easing inflation. Tech and AI leaders drove performance, though volatility surfaced amid mixed earnings results, cautious outlooks, and softening labor markets. Earnings growth expectations remained positive (but moderate), making fundamentals more critical than valuation expansion. We remain MORE favorable in this segment.

HFM Tactical Equity Positioning (Short Term)

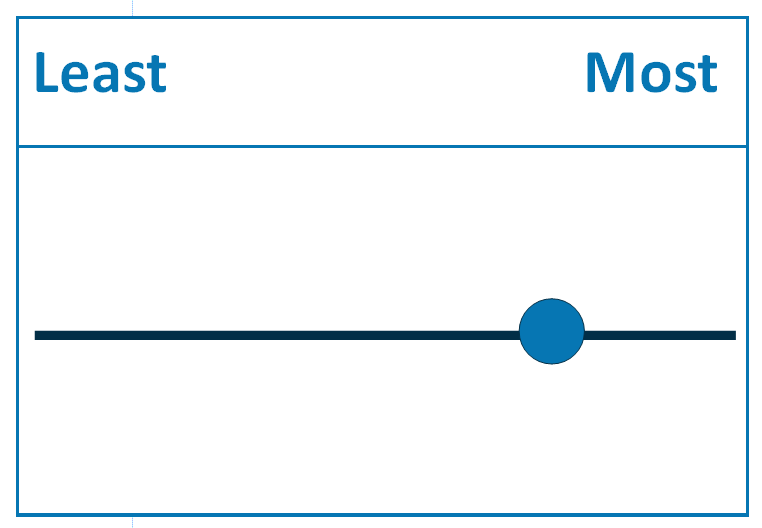

Large Cap

As the year closed, we have hit all-time highs on the S&P 500. Led by continued AI spending and strong earnings from companies beyond the top 10 largest companies in the index. Market valuations remain high, but we expect the market to continue to grow into those valuations. We remain MORE favorable in this segment.

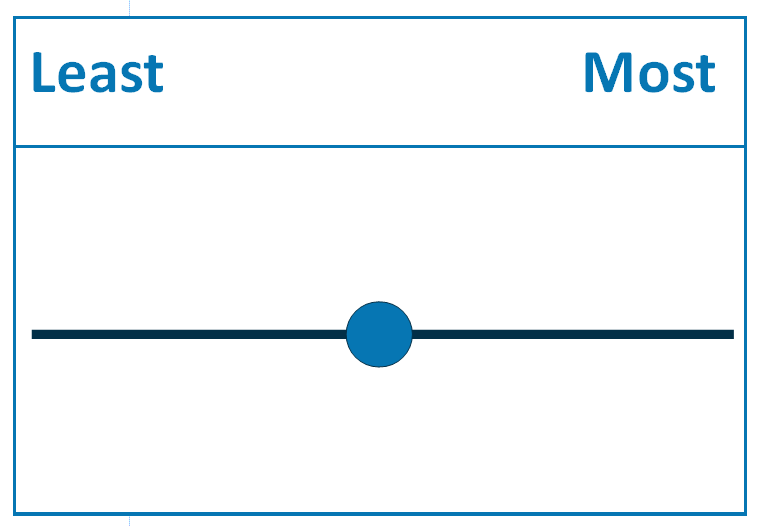

Small Cap

Small caps lagged large caps despite resilient economic data, with the Russell 2000 near highs but earnings revisions weakening and consensus EPS estimates declining more sharply than for large caps. The Federal Reserve lowered rates, which fueled a short-lived rally of small caps in Q4. We remain NEUTRAL on this segment.

Cutting Edge

The competitive AI landscape is shifting quickly as new winners are formed and old winners are now lagging. China has been developing its own technology and markets have been more discerning on who is a true AI innovator vs. companies with an AI facade. We are now MORE favorable on this segment.

International

After more than a decade of underperformance, international stocks are outperforming U.S. stocks on the weaker dollar. This outperformance could continue into 2026 especially if U.S. interest rates continue to be reduced by the Federal Reserve while the dollar weakens. We remain NEUTRAL on this segment.

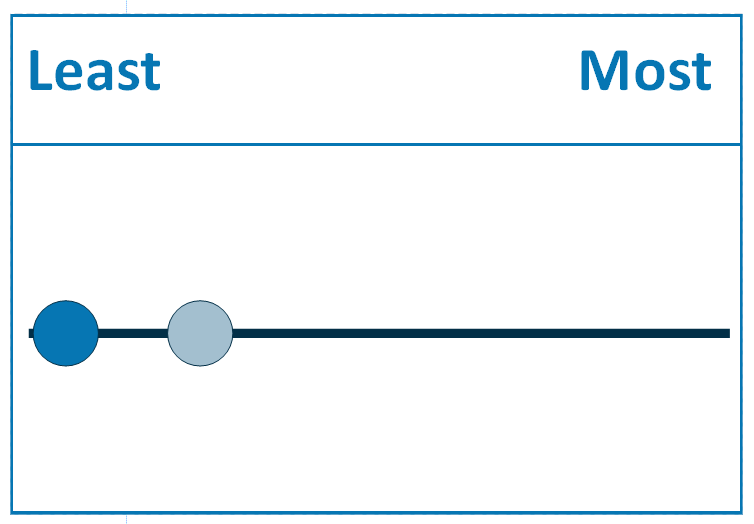

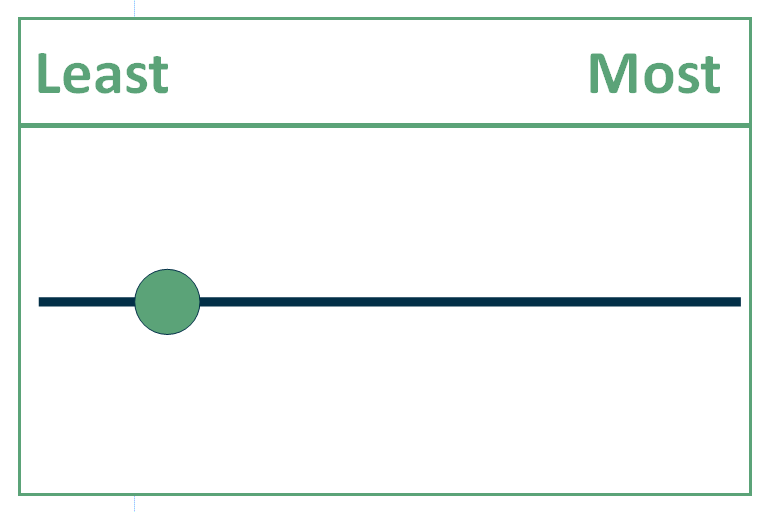

Hedged Equity

Although valuations remain high, the current market trend favors higher stock prices. One of the hedged equity investments reset in December so we plan to stay invested until further notice. Our exposure is limited and it’s likely these investments will be used tactically in the future. We are now LEAST favorable on this segment.

Fixed Income/Bonds Favorability

HFM Strategic Fixed Income Positioning (Long Term)

Fixed income performed well this year, delivering solid income while mitigating stock volatility during 2025. Overall yield levels continued to grind lower this quarter and are generally lower than where they began 2025. Among the factors that contributed to the yield decline are ongoing monetary policy easing with additional easing expected, the end of quantitative tightening, a cooling labor market, declining inflation expectations, and slower economic growth expected in 2026. Absolute yields remain elevated compared to what one received in the last 10 or 15 years, making them a desirable asset class. We maintain a MORE favorable outlook on Fixed Income.

HFM Tactical Fixed Income Positioning (Short Term)

Investment Grade Bonds

Investment Grade yield levels continue to remain attractive in absolute terms and in historical context. We continue to be biased toward sectors that offer greater compensation for interest rate, default, downgrade, and other risks. We maintain MORE favorable on this segment.

High Yield

High Yield borrowers in this market are financially healthier than historical averages but the yields for these bonds offer less in the way of return. They are priced with less of a buffer to an economic downturn and hence we remain LESS favorable.

Alternatives Favorability

HFM Strategic Alternatives Positioning (Long Term)

We echo our concerns from last quarter. While equity markets remain strong, they do look fully- to over-valued. If equity markets do not grow into their valuations, we can expect increased market volatility. Hence, we remain MOST favorable on Alternatives to help control for risk and provide a return in high-volatility environments.